Certax Accounting is presenting an overview of budget announcements to help taxpayers in the UK. This publication is providing valuable information about tax rates and income tax allowances, enabling taxpayers to effectively defend their tax planning on-time.

For more information of Tax rates and tax allowances, take a look below:

INCOME TAX RATES

Few days back we published WHY CASH FLOW FORECASTING IS IMPORTANT FOR YOUR BUSINESS? be sure to read that.

A- is representing the Rate on non-dividend savings income up to “£5,000″ A is 0% where taxable nonsavings income does not exceed £5,000.

B- is the dividend allowance that successfully taxes the first £2,000 dividends received at 0%. Dividends beyond this limit are taxed at 7.5%, this is for the basic and standard tax rate taxpayers. For higher rate taxpayers 32.5% and for additional and trust rate taxpayers the tax is 38.1%.

C- Basic rate band that is raised by gross Gift Aid donations and personal pension aids.

D- the Scottish income tax and rate bands apply to earned, pensions and property income of Scottish taxpayers. UK income tax rates and bands apply to other income like savings and dividend income, of Scottish taxpayers. From 6 April 2019, the Welsh Government will set the Welsh rate of income tax that applies to earned, pension and property income of Welsh taxpayers in addition to the UK rates less 10%. Moreover, the Welsh rate on income tax at 10% for 2019/20, will be the same as those applying in England and Northern Ireland.

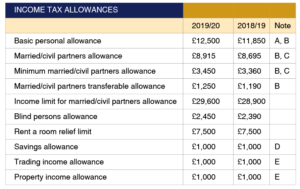

INCOME TAX ALLOWANCES

Confused? Get Free Consultation now!!!

A- Decrease by £1 for every £2 of income over £100,000.

B- Non-residents will not be allowed to personal allowances, in certain conditions.

C- Available to persons born before 6 April 1935. Relief limit is 10%. Reduced to minimum allowance by £1 for every £2 over the income limit. Minimum allowance reduced by £1 for every £2 income over £100,000 after applying personal allowance reduction.

D- £500 for a higher rate and £nil for additional rate taxpayers.

E- If gross income in excess of £1,000, a deduction of £1,000 instead of actual expenses is permitted.

Note High-income child benefit charge: 1% of the benefit per £100 of adjusted net income over £50,000: 100% of the benefit when adjusted net income is over £60,000.

PENSION CONTRIBUTIONS

Why don’t you try our online tax calculators to do the hard math work 🙂

A- Up to the lower of 100% of earnings or the maximum contribution. The maximum contribution is the annual allowance plus unused allowances from the three previous tax years. Up to £3,600 may be contributed regardless of earnings. Annual allowance reduced by £1 for every £2 income over £150,000 to a minimum of £10,000, and to £4,000 maximum if there are specific pension drawings.

CAPITAL GAINS TAX

See how our tax consultants help you out in the tax puzzles!

A- Gains on carried interest and chargeable residential property – 8% surcharge.

Note: Non-UK residents subject to capital gains tax (or corporation tax rate for companies) on the sale of UK residential property and, from 6 April 2019, non-residential property and certain disposals of interests in UK property rich entities.

Note: From 6 April 2019, certain disposals of UK land and buildings by non-residents must be reported and the tax rate for tax paid to HMRC within 30 days of sale. Similar rules will apply for certain disposals of residential property by UK residents from 6 April 2020.

INHERITANCE TAX

A- Additional residence zero rate band (RNRB) of £150,000 (2018/19 £125,000) for transfers of a main residence to direct children. NRB and RNRB for the estate of surviving wife/husband are increased by unutilised percentage of NRB and RNRB of the predeceased spouse. RNRB tapers away for estates over £2m.

B- Some lifetime gifts are taxed at 20%.

C- Tax rate decreased to 36% where up to 10% net chargeable estate is left for charity.

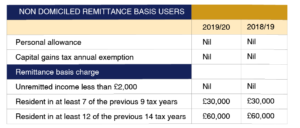

NON DOMICILED REMITTANCE BASIS USERS

Note: Certain returning former UK domiciled individuals, and non-domiciled individuals who have been resident in the UK in at least 15 of the previous 20 tax years, are treated as if UK domiciled for income tax, tax rate, tax allowances, capital gains tax and inheritance tax purposes.

NATIONAL INSURANCE CONTRIBUTIONS

If you are also working as a small business and wondering why outsource accounting services? See BENEFITS OF USING ACCOUNTING SERVICES

The first £3,000 of employer’s liability relieved by the employment tax allowances. From 6 April 2020, the employment allowance will only apply to companies with an NIC bill of less than £100,000. No employers NIC for employees aged under 21 (and apprentices up to age 25) on earnings up to £962 per week (the upper earnings limit).

Apprenticeship Tax rate at 0.5% payable on annual pay bills in surplus of £3m, net of £15,000 annual allowance.

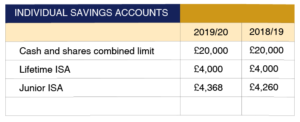

INDIVIDUAL SAVINGS ACCOUNTS

Note: For Buying ISA – deposit limit £1,200, plus up to £200 per month.

TAX EFFICIENT SAVINGS AND INVESTMENTS

A- Income tax relief at 50%.

B- Income tax relief at 30%.

C- £1.5m for enterprises up to 7 years old.

D- Up to £2m for ‘knowledge – intensive’ companies.

E- Capital gains tax deferral on gains reinvested in EIS qualifying investments.

F- Capital gains tax exemption on 50% of gains reinvested in SEIS qualifying investments.

PROPERTY STAMP TAXES

3% supplement to above tax rates for second properties and all purchases above £40,000 by corporates, discretionary and certain other trustees.

Residential properties in England and Northern Ireland purchased by non-natural persons (enveloped properties) for more than £500,000 incur a flat 15% SDLT rate unless relief is available.

First-time buyer exemption from SDLT for purchases up to £300,000 and for the first £300,000 of purchases up to £500,000.

First-time buyer relief from LBTT for the first £175,000 of relevant property purchases.

Residential Leases

England and Northern Ireland – 1% on the present value of rents £150,001 to £5m, 2% above £5m.

Scotland – 1% on the present value of rents over £150,000.

Wales – 1% on the present value of rents £150,000 to £2m, 2% above £2m.

Note: The time limit for filing a stamp duty land tax return and paying the stamp duty land tax liability is reduced from 30 to 14 days for transactions with an effective date after 1 March 2019

ANNUAL TAX RATE ON ENVELOPED DWELLINGS

Note: Prior to 1 April 2019, gains on disposals of property within the Annual Tax Rate on Enveloped Dwellings regime subject to capital gains tax at up to 28%.

CORPORATION TAX AND DIVERTED PROFITS TAX

A- Withheld at the source.

B- Applies to profits of large entities diverted from the UK as a result of an avoided permanent establishment or transactions which lack economic substance.

We presented a list of 6 TAX DEDUCTIONS FOR SAVVY SMALL BUSINESS OWNERS to assure their business is tax-efficient.

PATENT BOX

A- Nexus based regime operates from 1 July 2016. Previous regime available until 2021 if opt-in the election made for patents registered by 30 June 2016.

RESEARCH AND DEVELOPMENT TAX ALLOWANCE RELIEF

A- Additional (enhanced) tax deduction available for qualifying R&D expenditure.

B- From 1 April 2020, the payable R&D tax credit in any tax year is restricted to three times the company’s total PAYE income tax and NIC liability for the year.

C- Taxable credit available on qualifying R&D expenditure.

CAPITAL TAX ALLOWANCES

A- Maximum annual investment allowance £1m pa from 1 January 2019 to 31 December 2020 (£200,000 pa to 31 December 2018 and from 1 January 2021).

B- Reducing balance.

C- Available for: research and development (no time limit); enterprise zone (assisted areas) until designated dates between 31 March 2020 and 16 March 2024; energy saving and environmentally beneficial (water efficient) technologies until 31 March 2020/5 April 2020; brand new low emission cars and gas refuelling stations until 31 March 2021; zero-emission goods vehicles until 31 March 2021/5 April 2021; and electric vehicle charge points until 31 March 2023/5 April 2023.

D- Expenses on non-residential structures and buildings on construction contracts entered on 29 October 2018 and so on.

Few weeks back we discussed TAX DEBATE: COMPANY CAR OR CAR ALLOWANCE?

VALUE ADDED TAX

A- Taxable turnover calculated through the reference to the last 12 months or next 30 days.

DIGITAL SERVICES TAX

STAMP DUTY

Consideration on shares over £1,000 | 0.5%

AUTHORISED MILEAGE RATES

CAR AND FUEL SCALE BENEFITS

Notes:

Electric Vehicles Benefit 16%.

Diesel vehicles meeting the RDE2 standard will be discharged from diesel supplement and the above petrol rates apply for such vehicles.

Recent Comments